Subscribe to our newsletter and get the latest resources sent to your inbox.

FeedMob’s Mobile Ad Supply: Insights from 2022

9 MIN READ

January 19, 2023

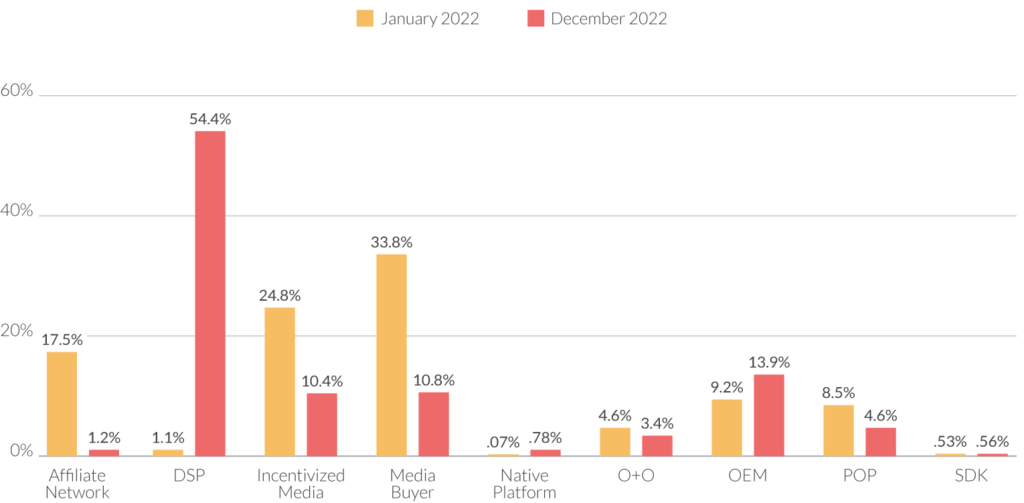

It’s a new year, so our team has gathered updated insights into where our clients are spending their budgets and which mobile ad supply categories are gaining popularity with user acquisition managers. Overall, we’ve seen a dramatic increase in programmatic expenditure and steady usage of supply partners across incentivized media, pop, owned and operated or direct publishers (O&O), native ads, and original equipment manufacturers (OEM) or preloaded inventory. (Check out our blog post that explains inventory supply types to learn more about these categories.)

Supply Comparison: January 2022 vs. December 2022

Programmatic is having a moment, but other mobile ad inventory remains strategically valuable

Spending on programmatic ads has increased heavily across our client book — not just due to the quality of traffic this category provides but also because acquisition costs were competitive. And it should be mentioned that in a post-SKAN world, programmatic partners were able to implement SKAN IDs, thereby receiving postbacks and providing clear attribution to our clients. In other words, intrepid clients, ready to test SKAN-friendly inventory, embraced programmatic.

OEM’s organic experience for the win

Interestingly, even though the other categories mentioned at the beginning of this post have seen a decrease in spending due to programmatic demand, they remained popular choices across all verticals. There is a variety of reasons for this. For instance, OEM traffic provides users with a more organic experience as the ads are preloaded on the user’s devices. With the right strategy and audience targets (specific to devices, carriers, and so on), OEM can yield high conversion rates at a lower cost. Similarly, native platforms allow for a higher scale of trust among users due to the nature of the ad design and its match to the content of the paid media source.

Cost-effective solutions that drive value

Pop and media buying partners faired well last year due to the extreme cost-effectiveness that drove value in specific client verticals. While pop ads can be viewed as intrusive, they allow for a relatively low-cost supply with high visibility and user interaction. Partners with media buying capabilities were a critical component of our supply mix offering in 2022 as they provided specialized insight into finding new sources of untapped inventory. Of course, it’s important to hire an agency that can perform due diligence on media buyers and ensure that truly high-quality users are delivered.

Reaching new users with new sources of inventory

Direct (O&O) and incentivized media partners added value to clients looking to expand in new marketplaces. O&O provides clean and trusted traffic with targeted audiences that can benefit specific clients. Rewarded media delivers users who are highly engaged and opt-in to being rewarded – a great benefit that can target valuable users and provide high ROAS to the client.

Overall, 2022 was a good year for programmatic supply and those agencies and supply partners who are enabling themselves in a post-privacy world. While trends can tell us a lot, finding the correct media mix for each client is absolutely integral to success, as even across one supply category, there is a myriad of checklist items, tests, and set-ups that must be addressed to ensure client campaigns are successful.

Agencies and partners should equip themselves with more than expertise in the mobile space. Being nimble enough to rapidly develop technology and tools that help clients in the ever-changing mobile landscape is essential in a constantly changing mobile advertising landscape.

Posted: January 19, 2023

Category: Data Trends, Mobile Insights Blog

Tags:

Stay Updated.

SERVICES

RESOURCES

CONNECT