Subscribe to our newsletter and get the latest resources sent to your inbox.

FeedMob’s Mobile Ad Supply: Insights from 2023

9 MIN READ

January 9, 2024

Mobile performance marketers know that ad spending shifts with industry priorities. When user acquisition is all that matters, spending tends to focus on channels that maximize installs. If down-funnel activities are a priority, marketers may shift their spending to find higher-quality users at a lower CPA. This year, we saw clients focus on channels with the best chance of achieving more efficient CPA targets — their spending reflects that.

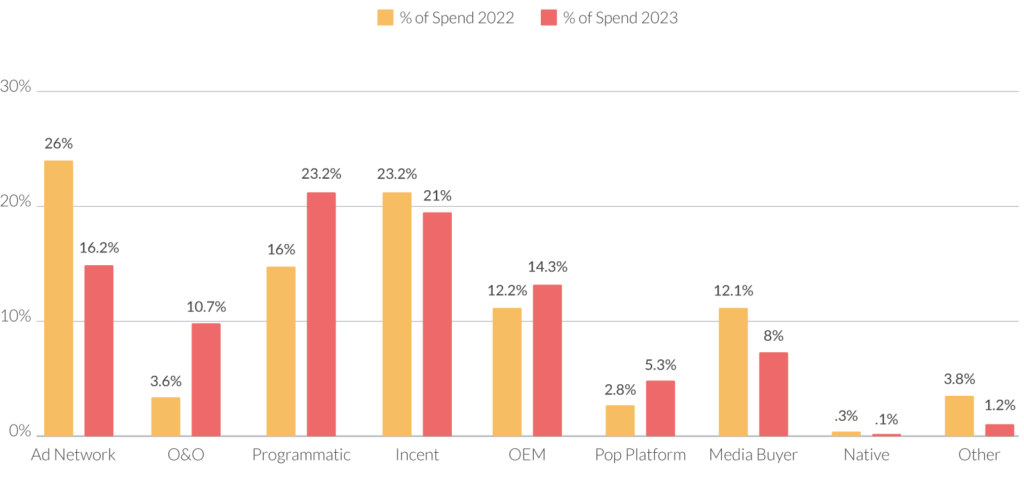

Last year we saw Programmatic traffic run away with a sizable percentage of the year’s mobile ad spend. This year, however, we’re seeing a more even spread across mobile ad supply categories. That said, our data tells us that Programmatic, OEM, and Owned & Operated (O&O) were the only categories where the percentage of spend grew year-over-year (YoY), continuing to underline the importance of these channels for apps looking to expand their user acquisition efforts beyond search and social. Incent also had a strong year, even as its percentage of ad spending dipped slightly. Read on to learn more about why our client book of global apps focused their spending on these channels.

Supply Comparison: 2022 vs. 2023

Programmatic and OEM continue to prove valuable and scalable

Many of the same reasons Programmatic was popular last year remain true in 2023. The quality of traffic, high level of transparency for optimization, competitive acquisition costs, reach and capacity for scale, and the ability to implement SKAN make this a popular choice among our clients.

Meanwhile, OEM traffic promotes the app directly on the device to provide an ad environment that integrates smoothly with everyday phone use. Perhaps even more importantly, it lets advertisers target massive yet selected audiences by device and carrier, resulting in a high conversion rate at minimal cost.

O&O and Incent have a chance to shine

O&O inventory is an excellent source of clean and trusted traffic with targeted audiences. It can often provide a contextual experience that allows our clients to find new users when they’re likely to take action. This proves especially valuable for clients looking to expand into new markets or double down on user groups where internal data analysis finds high value. The cherry on top is that they can run SKAN campaigns most of the time.

Incent or rewarded traffic, while wildly different from O&O, has a similar reputation for delivering efficient CPAs. Someone who opts in to receive rewards tends to complete key actions early in app usage at a higher rate than a non-incentivized user. However, incent inventory can have lower retention, necessitating setting suitable CPA targets and focusing on managing the appropriate rates relative to LTV. Incent campaigns also come in various formats, including burst campaigns that target a specific install goal over a short period, letting us get creative with new ways to meet a client’s goals and multi-reward or play-to-earn programs that aim at building the habits for the right groups of users. It’s also a great add-on to the existing media mix to create compounding positive effects to attract more potential organic users.

Overall, 2023 was a year for efficiency. App marketers focused on efficiency and profitability, so we saw downward pressure on CPA targets. While we expect interest rates to decrease — making it easier for our clients to secure loans and expand budgets — the trend in 2024 will continue to be CPA efficiency. However, we expect CPAs to rise slightly and to see a greater interest in testing new channels as the U.S. economy shows signs of resilience and growth. With that in mind, we also forecast more monetization efforts from app developers and OEMs, ultimately leading to increased diversity in the available supply. As a result, we expect advertisers to continue to focus on buying more unique inventory that meets their CPA targets.

Posted: January 9, 2024

Category: Data Trends, Mobile Insights Blog, Mobile Performance Strategies

Tags: CPA, strategy, supply

Stay Updated.

SERVICES

RESOURCES

CONNECT